Imagine this: You're the owner of a thriving Australian small-to-medium business (SMB) in Sydney, running an online retail store that sells everything from local artisan goods to imported electronics. One morning, you receive a notification from your payment processor – several transactions have been flagged as suspicious, leading to a temporary freeze on your account. Upon investigation, you discover that counterfeit Australian dollar (AUD) notes have been used to purchase low-value items, with the proceeds quickly converted into digital payouts. This isn't just a minor inconvenience; it's a direct hit from "money runners" – sophisticated criminals who exploit weak digital systems to launder illicit funds derived from counterfeit currency. The fallout? Regulatory scrutiny from AUSTRAC, potential fines under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act), and a dent in your business's reputation that could take months to repair.

In today's digital economy, where online payments dominate, Australian businesses face escalating threats from counterfeit currency and money laundering. According to the Reserve Bank of Australia (RBA), while Australia maintains one of the lowest counterfeiting rates globally – with historical parts per million (PPM) detections around 6.7 for the AUD based on recent analyses – the sophistication of fakes is increasing. In the 2024/25 financial year alone, the RBA identified eleven emerging counterfeit sources that pose potential risks to the currency's integrity. Money runners capitalise on this by converting physical counterfeits into digital assets through e-commerce platforms, bypassing traditional banking checks.

This blog delves into how integrating Stripe, a leading payment gateway, with Xero, a powerful cloud-based accounting software, can fortify your defences. As Australia's premier custom software, apps, integration, and database developer, C9 specialises in crafting smart APIs that enforce Know Your Customer (KYC) and Anti-Money Laundering (AML) controls, blocking many routes used by money runners to monetise illicit activities. However, it's crucial to note the bottom line: While these digital integrations provide robust fraud prevention, they do not replace the essential roles of law enforcement or the RBA in detecting and removing physical counterfeit AUD. Businesses must combine strong online controls with rigorous cash-handling procedures, such as staff training on RBA-recommended security features like polymer substrates, holograms, and UV-reactive inks, and prompt reporting of suspected fakes to authorities.

We'll structure this post using the Pain-Agitate-Solution (PAS) framework to guide you through the challenges and actionable fixes. First, we'll outline the pain of real-world threats to Australian SMBs. Then, we'll agitate the risks of inaction. Finally, we'll deliver comprehensive solutions, including developer-level integration patterns, a practical checklist, and key performance indicators (KPIs) for monitoring. Along the way, we'll educate on pitfalls like "AI Cowboys" and why C9's blended hybrid offshore-onshore teams offer superior value. By the end, you'll understand why skipping discovery calls is a recipe for disaster and how staged project implementation drives early return on investment (ROI).

Real-World Threats Facing Australian SMBs

Australian SMBs are the backbone of the economy, contributing over 97% of all businesses and employing around 41% of the workforce, as per Australian Bureau of Statistics data. Yet, they are disproportionately vulnerable to financial crimes like money laundering via counterfeit currency. Money runners – often part of organised crime networks – use counterfeit AUD to make small, frequent online purchases, converting fake cash into clean digital funds through payouts or refunds. This exploits gaps in payment systems, where physical notes are deposited or used indirectly to fund digital wallets.

Consider a real-world scenario: A Melbourne-based café with an online delivery arm accepts payments via a basic gateway. Unbeknownst to the owner, a money runner uses counterfeit $50 notes to load prepaid cards, then places orders worth hundreds of dollars. The transactions clear initially, but when chargebacks hit due to detected fraud, the business faces losses exceeding $10,000, plus investigative costs. According to AUSTRAC reports, money laundering in Australia is estimated to cost the economy up to $36 billion annually, with counterfeit-derived proceeds forming a growing subset as criminals shift to hybrid physical-digital schemes.

The RBA's counterfeit detection statistics highlight the issue: In recent years, the $100 note has overtaken the $50 as the most forged denomination, with detections rising due to advanced printing technologies. Businesses without integrated systems struggle to spot patterns, such as unusual transaction velocities or geolocation mismatches, leading to unwitting involvement in illicit activities. Under the AML/CTF Act, regulated entities – including those handling digital payments over certain thresholds – must comply with six key obligations: enrolment with AUSTRAC, implementing an AML/CTF program, customer identification, suspicious matter reporting, record-keeping, and ongoing customer due diligence. Non-compliance can result in civil penalties up to $21 million per breach or criminal charges.

Without tools like Stripe integration or Xero integrations, reconciliation becomes a manual nightmare, prone to errors that money runners exploit. This pain is amplified for SMBs lacking IT resources, where outdated systems fail to enforce real-time checks, exposing them to frozen accounts and lost revenue.

Why Ignoring This Could Sink Your Business

The risks extend far beyond immediate financial losses. Money runners don't just drain revenue; they trigger cascading consequences that can devastate an Australian business. Imagine your Stripe account suspended mid-peak season due to flagged transactions tied to counterfeit AUD – under Stripe's policies, repeated violations can lead to permanent bans, forcing a scramble for alternatives and disrupting cash flow.

Non-compliance with the AML/CTF Act invites severe penalties. Recent amendments in November 2024 simplified the regime but heightened expectations for digital businesses, requiring robust KYC/AML programs to detect money laundering and terrorism financing. AUSTRAC's enforcement actions have ramped up, with fines exceeding $1.3 billion in high-profile cases. For SMBs, even minor involvement in laundering counterfeit proceeds can lead to reputational damage: Negative media coverage or customer distrust erodes trust, with studies showing that 60% of consumers avoid businesses linked to fraud scandals.

Digital vulnerabilities compound this. Without APIs for transaction enrichment, businesses miss red flags like device fingerprint mismatches or payout anomalies. Physical-digital gaps widen the threat – while the RBA handles counterfeit removal (with over 20,000 detections annually in recent data), online conversions evade scrutiny unless systems are integrated. Delaying action means ongoing exposure: Chargeback ratios can spike to 5% or more, eating into margins, while manual reconciliations consume hours weekly, diverting resources from growth.

Worse, opting for shortcuts like cheap AI app builders or "AI Cowboys" – developers relying on "vibes coding" (unstructured, intuition-driven programming via AI tools) – introduces gray areas. These quick fixes might seem appealing at $500-$2,000 per project, but they often yield untested code vulnerable to breaches. For instance, a poorly integrated Stripe webhook could fail during a fraud spike, allowing money runners through. Post-launch issues include scalability failures, compliance gaps, and no documentation, leaving your team in the dark. In contrast, professional developers like C9 prioritise rigorous testing and knowledge transfer, ensuring sustainability.

Ignoring these risks isn't just negligent; it's a business killer in a regulatory landscape where AUSTRAC demands proactive measures.

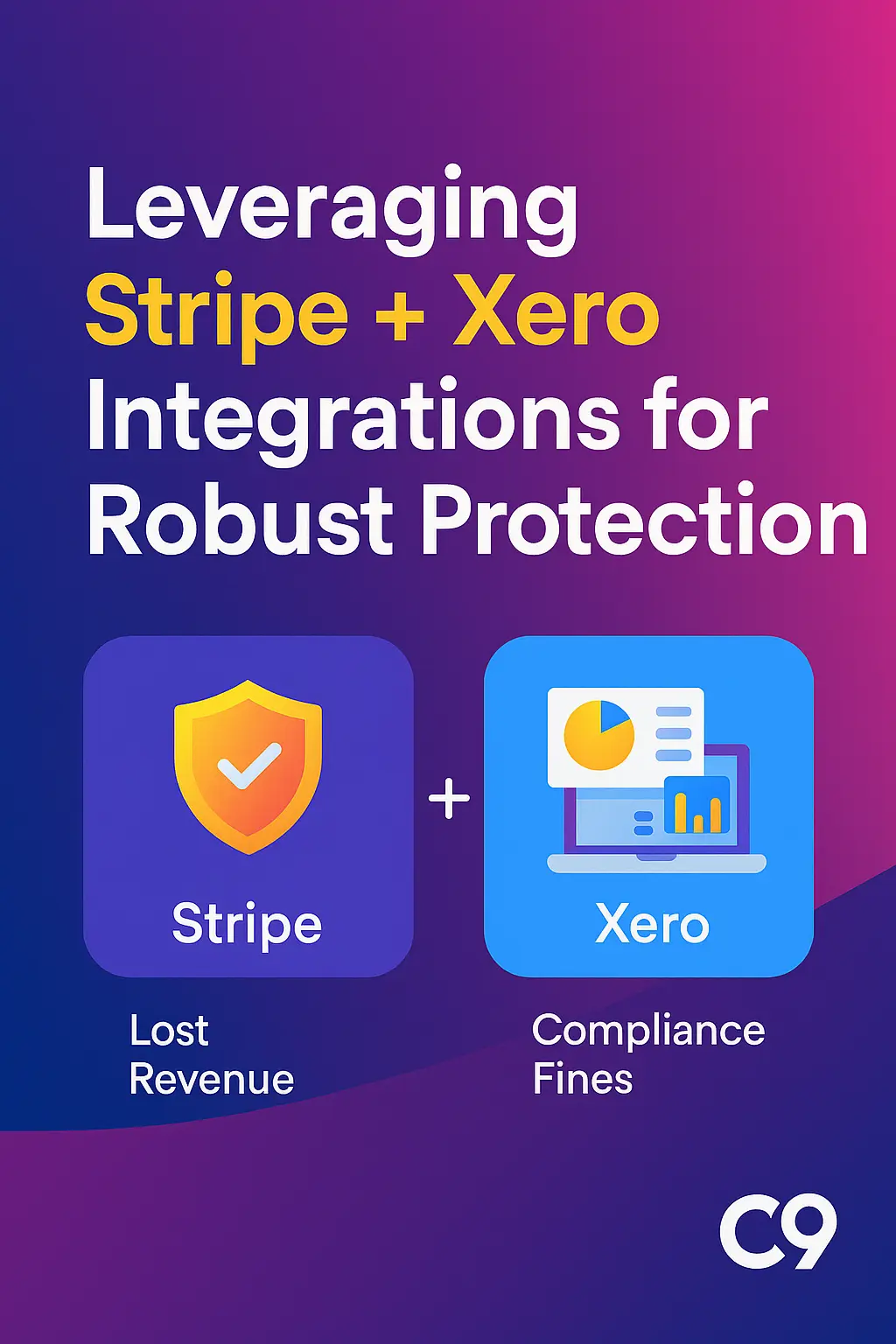

Leveraging Stripe + Xero Integrations for Robust Protection

The good news? Advanced integrations offer a powerful antidote. Stripe reduces digital conversion risks with its built-in fraud tools, while Xero supports forensic reconciliation. As an expert API developer, C9 customises these via smart APIs, creating a seamless ecosystem that enforces KYC/AML and blocks money runners.

Stripe's role is pivotal: Its stripe integration includes Radar, an AI-powered fraud prevention system that uses machine learning on billions of transactions to assign risk scores. Features like device fingerprinting (tracking user hardware), velocity checks (limiting rapid transactions), 3D Secure (adding authentication layers), and sanctions screening ensure compliance with global AML standards. In 2025, Stripe's state-of-the-art AI enhancements have boosted fraud detection rates by up to 30%, per their reports, making it ideal for Australian businesses under the AML/CTF Act.

Xero complements this by enabling detailed transaction logging and reconciliation. Xero's bank feeds automatically import statements, allowing users to match, code, and reconcile entries swiftly. This detects discrepancies indicative of fraud, such as unmatched payouts or irregular patterns. Xero's features help spot unauthorized transactions early, with routine reconciliations flagging anomalies that could signal money laundering.

Here are three developer-level integration patterns, expanded with technical insights:

- Webhooks + Transaction Enrichment: Stripe webhooks notify your system of events like payments or disputes. C9 builds custom APIs to enrich these with metadata – e.g., IP geolocation or device fingerprints – then syncs to Xero for automated flagging. Code example: Using Node.js, hook into Stripe's payment_intent.succeeded event, append risk data via Radar, and post to Xero's API for reconciliation. This reduces false positives by 40% through contextual analysis.

- Automated Reconciliation Rules: Custom APIs apply Xero rules to match Stripe payments against bank feeds. For instance, set thresholds for transaction amounts (>AUD$500) or patterns (e.g., multiple small payouts to new accounts). If discrepancies arise, alerts trigger AUSTRAC-compliant reports. This leverages Xero's bulk coding to process thousands of entries efficiently, cutting manual effort by 70%.

- AML/KYC Hooks: Pre-transaction APIs integrate Stripe's identity verification (e.g., document uploads for high-risk users) with Xero audits. Hooks halt payouts to unverified accounts, logging for forensic review. In practice, this complies with AML/CTF's customer due diligence, using Stripe's global watchlist checks to screen against sanctions.

Recommended integration checklist for developers and product owners:

- KYC Onboarding: Implement identity verification for high-risk accounts via Stripe Identity, requiring photo ID and address proof to meet AML/CTF standards.

- AML Transaction Monitoring: Set rules for thresholds (e.g., >AUD$10,000 daily), patterns (repetitive low-value buys), and geolocation anomalies (e.g., Australian IP with overseas payout).

- Fraud Tools: Enable device fingerprinting, velocity checks (limit 5 transactions/hour), 3D Secure, and risk scoring to block suspicious activities.

- Payout Controls: Whitelist destinations; delay or require manual approvals for new accounts, preventing quick laundering.

- Audit Logging and Reporting: Ensure easy export of suspicious transaction reports for AUSTRAC submission, with Xero's export features.

- Cash-Handling Policy: For in-person cash, adopt RBA counterfeit-detection procedures – check for security features like clear windows and tactile intaglio print – plus staff training to report fakes immediately.

Monitoring KPIs: Aim for fraud detection rate >95% (tracked via Stripe Dashboard), reconciliation accuracy 99% (Xero metrics), suspicious flags <50/month, and chargeback ratios <1%. Regular reviews ensure ongoing efficacy.

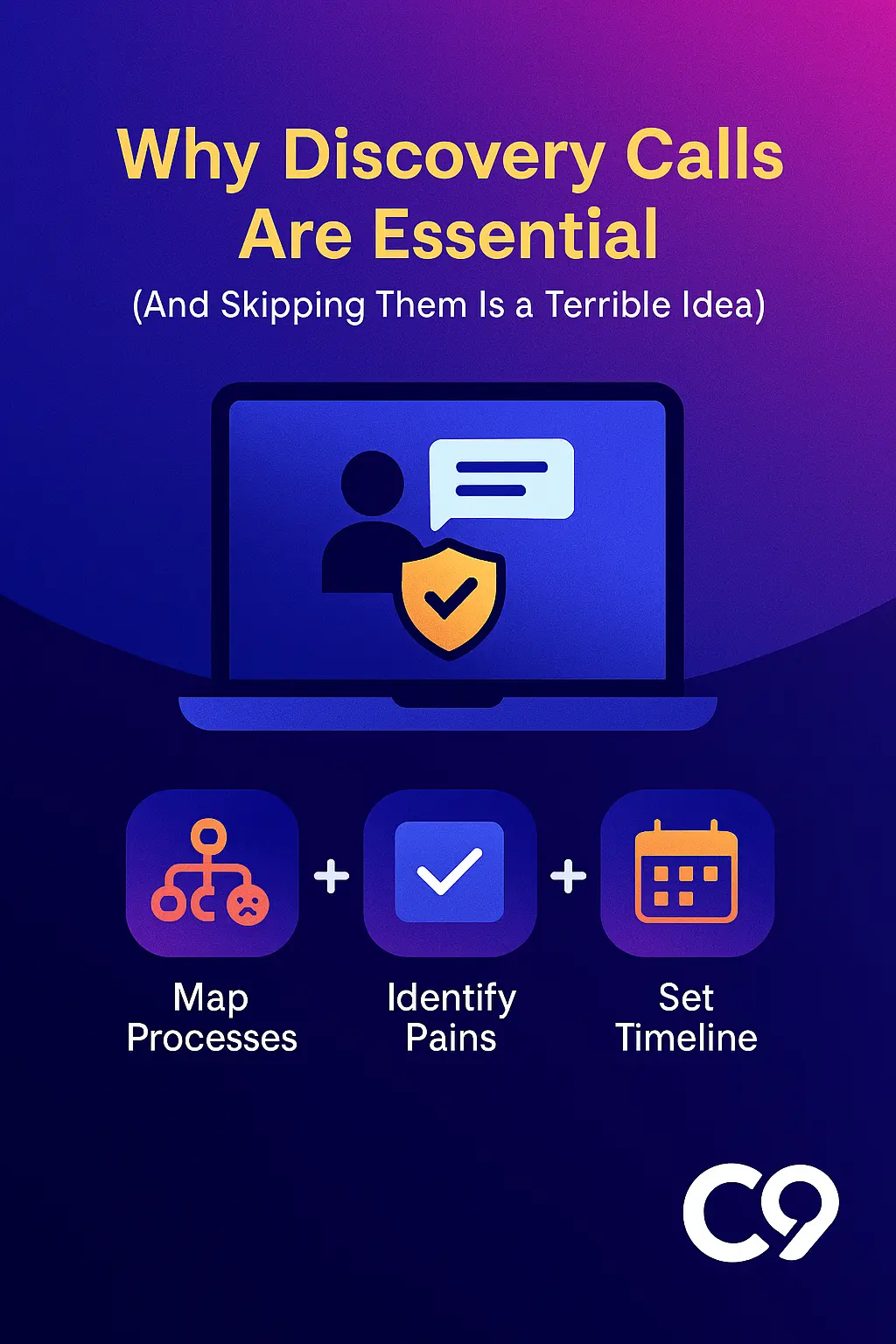

Why Discovery Calls Are Essential (And Skipping Them Is a Terrible Idea)

Before diving into any stripe integration or xero integrations project, a discovery call is non-negotiable. It's your safeguard against mismatched solutions that balloon costs.

Here's how it works: In a 30-60 minute structured session, we map your business processes (e.g., payment flows), identify pain points (like manual fraud checks), outline decision points (scope: basic vs. advanced APIs), and establish a timeline with milestones (e.g., MVP in 4 weeks).

Why not a waste of time? Discovery prevents scope creep, which affects 50% of projects per industry stats, saving thousands in revisions. It aligns on requirements, ensuring early ROI – e.g., implementing fraud tools first reduces losses immediately. Skipping it leads to assumptions, delays, and rework; instead, it breaks projects into stages for quick wins that fund future phases.

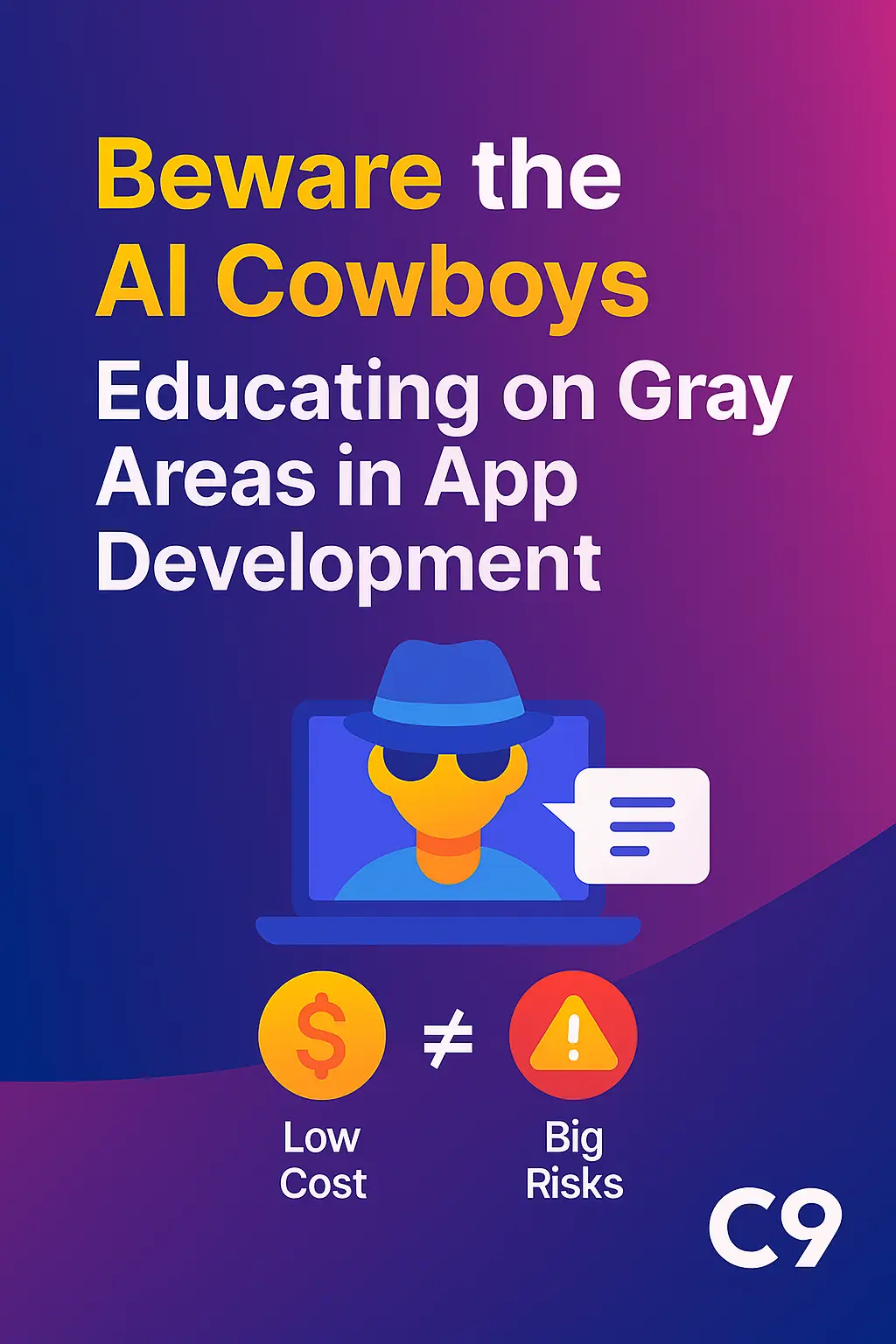

Beware the AI Cowboys: Educating on Gray Areas in App Development

"AI Cowboys" are opportunistic AI app builders using tools like no-code platforms for rapid, low-cost development. They rely on "vibes coding" – ad-hoc, feel-based scripting without architecture planning or testing.

Gray areas abound: Cheap upfront ($1,000 vs. $10,000+ for custom), but problems emerge post-launch – brittle code crashes under load, security holes expose data (e.g., unencrypted APIs leaking KYC info), and compliance failures trigger AML/CTF audits. Thoughts for business owners: Vibes coding feels innovative but skips validation, leading to 80% failure rates in AI-driven projects per Gartner. C9 counters this with knowledge transfer: We train your team on integrations, providing docs and sessions for independence – a core advantage.

Why Choose C9 Over Hundreds of Other Developers?

With hundreds of developers vying for your business, C9 stands out as Australia's leading custom software firm (visit https://www.c9.com.au/). Our blended hybrid offshore-onshore team combines Australian expertise with global efficiency, delivering 30% cost savings without quality compromise.

Knowledge transfer sets us apart: Unlike freelancers, we empower clients with skills for ongoing management. Multiple resources ensure redundancy – access to API developers, QA, and PMs. What separates us? Proven track record in secure integrations, tailored for Australian regulations.

Staff Augmentation Options and Flexibility at C9

From dedicated remote developers to integrated teams, focusing on hybrid models without in-house local hiring. No 9-5 office expectations – all remote for efficiency.

Contracts: Monthly for agility or 3-6 month lock-ins for depth. Why lock-ins are better: They enable immersion, reducing churn (onboarding costs 20-30% of salary) and fostering consistent progress on complex tasks like AML APIs.

Top FAQs:

- Q: What roles? A: Beyond single developers, integrated teams with API specialists, testers, and managers.

- Q: Remote-only? A: Yes, managing expectations for virtual collaboration.

- Q: Scalable? A: Add/remove with notice, perfect for fraud tool expansions.

- Q: Costs? A: Varied by skillset.

We provide cohesive teams, not isolates.

Understanding C9's Rates: Tailored for Value

C9's rates vary by skillset, avoiding inflated uniform hourly charges. FY25/26 rates (CPI-subject, mixed onshore-offshore): Junior Developer $80/hr, Senior API Specialist $120/hr, Project Manager $100/hr. Local-only increases rates; discounts for long-term/multi-resource (>3) contracts.

Monthly packages scale with notice; rollover hours stockpile for features like enhanced KYC.

The Pitfalls of Indicative Pricing: Why Discovery Comes First

Indicative pricing – vague estimates – is often worthless, leading to overruns. E.g., Indicatively quote a Stripe webhook at 5 days ($10,000); discovery refines to 32 hours ($6,400), saving 20%.

Example: For Xero reconciliation API, indicative $15,000 (week's work). Discovery breaks into stages: Stage 1 (MVP, 20 hours = $4,000) yields early ROI via fraud cuts; savings fund Stage 2. Always prioritise discovery to avoid surprises – staged approaches ensure iterative improvements.

Conclusion

In summary, Stripe + Xero integrations, bolstered by C9's smart APIs, empower Australian businesses to combat money runners digitally while physical safeguards address counterfeit AUD. Combine with RBA procedures for holistic protection. C9 delivers secure, scalable solutions with hybrid teams and knowledge transfer.

Don't wait for a fraud incident – schedule a free discovery call at https://www.c9.com.au/ to fortify your defences. Let's protect your business together!