In Australia's booming e-commerce market—projected to exceed A$80 billion by 2026—every percentage point in payment fees can erode your hard-earned profits. As a business executive dealing with high operational costs, outdated systems, or competitors gaining tech edges, you're right to scrutinize options. PayPal and Stripe dominate, but with 2025 regulatory shifts from the Reserve Bank of Australia (RBA), choosing wisely isn't just about convenience—it's about safeguarding efficiency and growth.

At C9, we've partnered with over 500 Australian SMBs to integrate these gateways seamlessly into custom software ecosystems. Let's break down the 2025 landscape to help you decide which saves more.

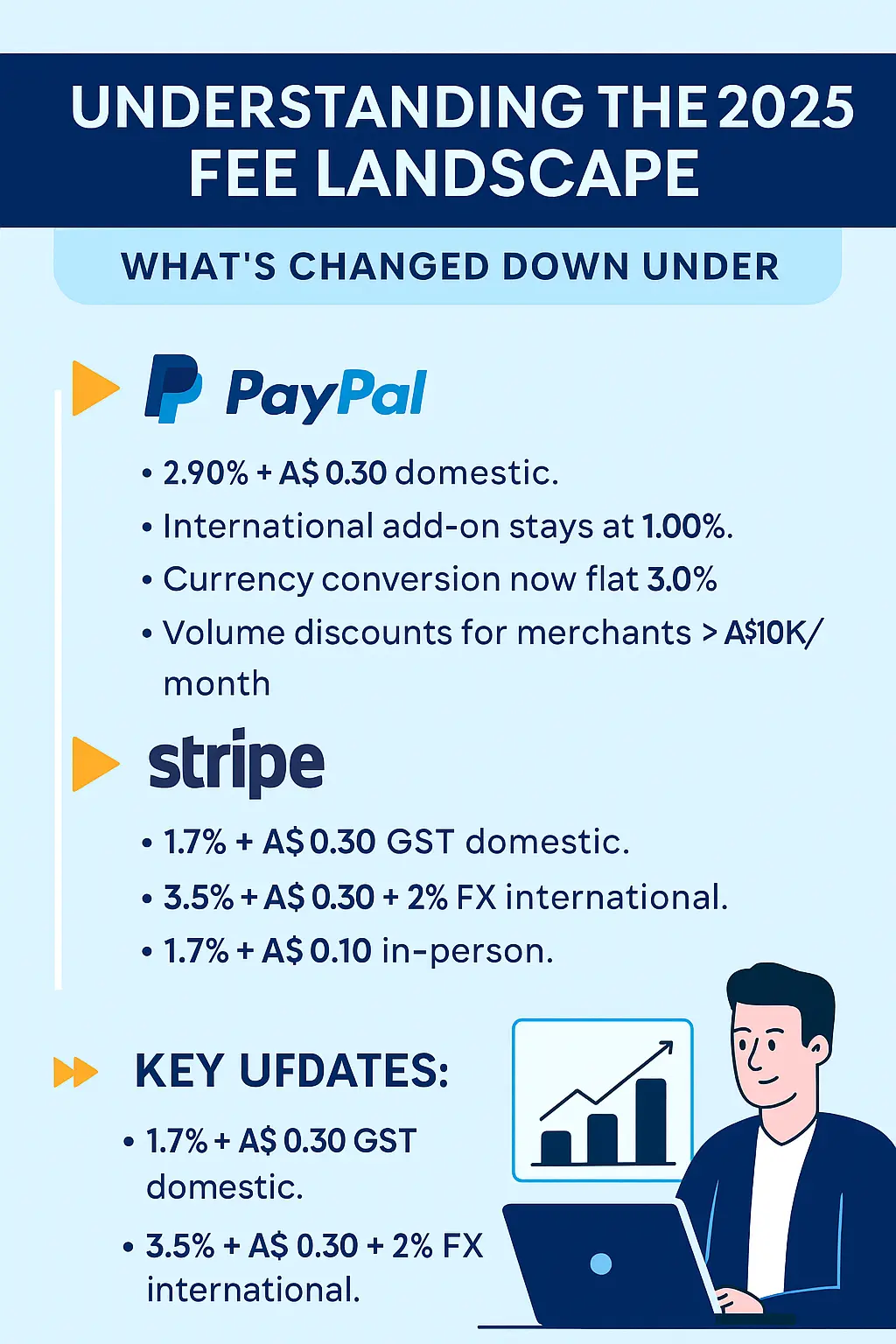

The 2025 Fee Landscape: Regulatory Changes Impacting Your Bottom Line

Rising costs and poor integrations are agitating enough—now add RBA's surcharging reviews and potential debit bans by 2026. These could increase transparency but hike base fees for non-compliant gateways. PayPal adjusts for cross-border trade; Stripe refines volume discounts amid 15% export growth in 2024. Key updates include:

- BNPL regulations (effective June 2025) requiring stricter compliance.

- Function-based licensing to curb hidden charges.

(Source: RBA Payment Systems Review, 2024)

Detailed Fee Breakdown: PayPal vs Stripe

Hidden fees can quietly drain revenues, aggravating missed growth targets. Here's a side-by-side comparison for Australian businesses:

| Transaction Type |

PayPal Fees (2025) |

Stripe Fees (2025) |

Potential Annual Savings with Stripe* |

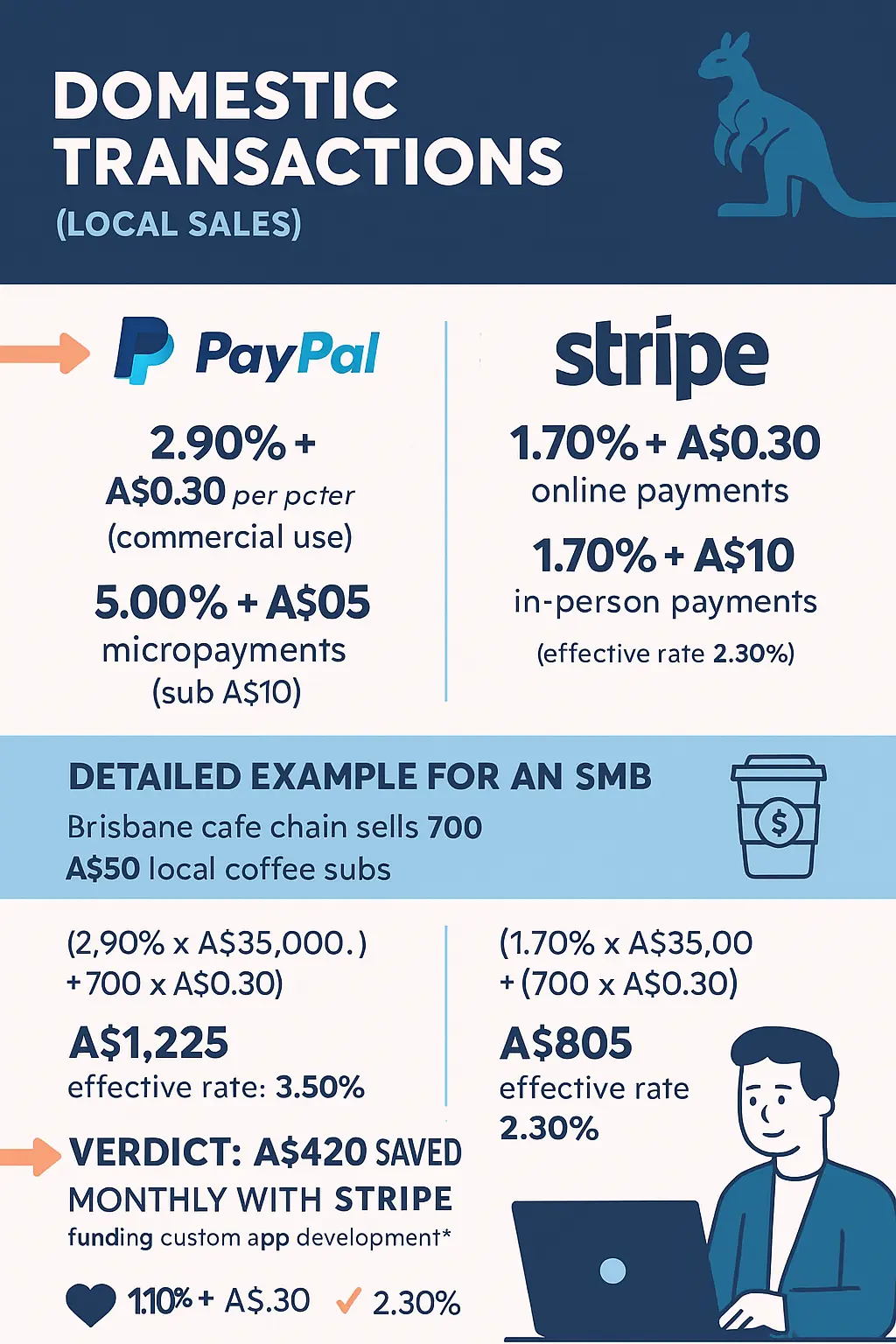

| Domestic (Card) |

2.90% + A$0.30 |

1.70% + A$0.30 |

A$5,040 (on A$35,000 monthly volume) |

| International (Card) |

3.90% + A$0.30 + 3.0% conversion |

3.50% + A$0.30 + 2% conversion |

A$7,560 (on A$45,000 monthly volume) |

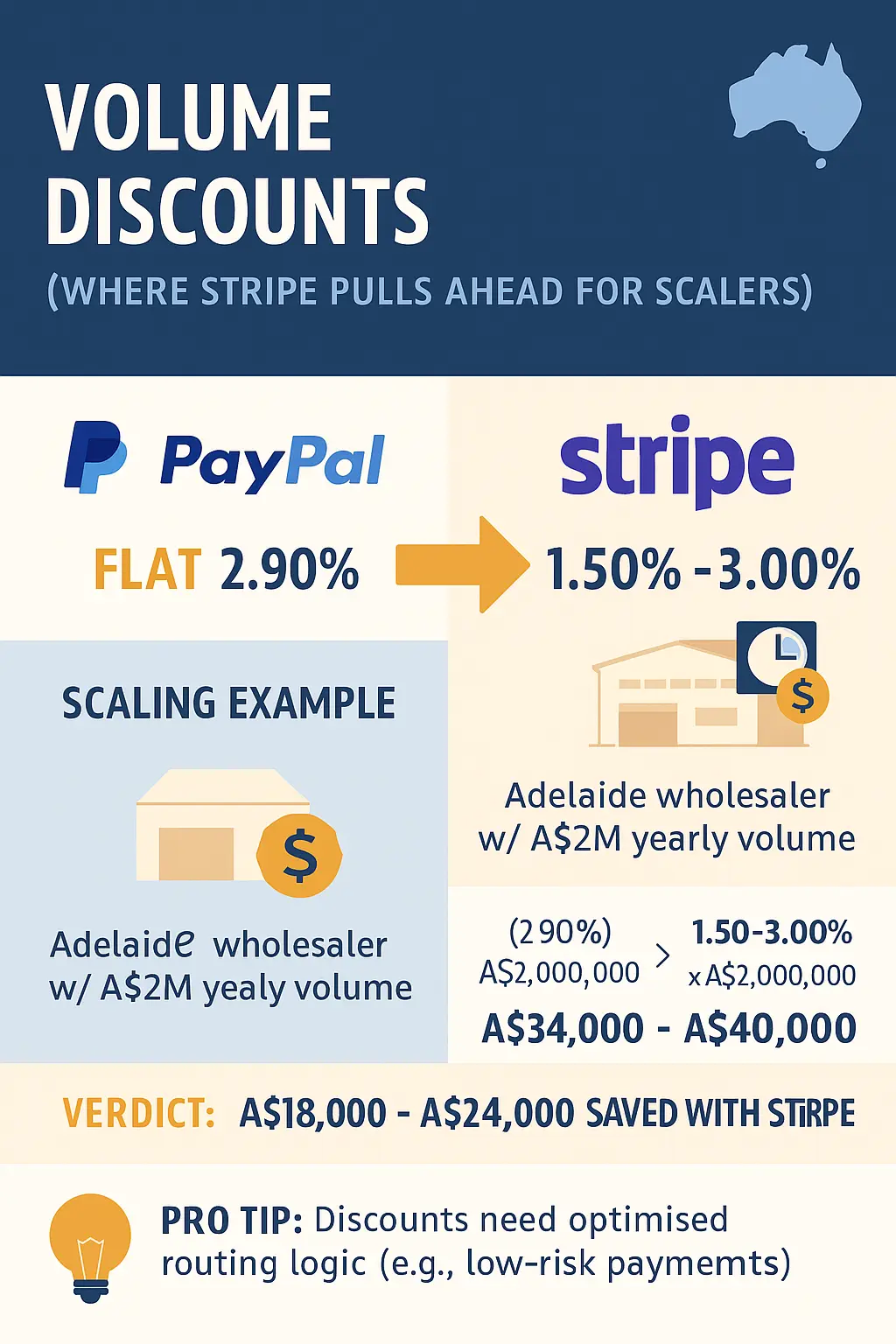

| Volume Discounts (A$1M+ annual) |

Negotiable to 2.60% |

Tiered: 1.5% at A$2M |

A$18,000–A$24,000 |

| Micropayments (<> |

5.00% + A$0.05 |

Standard rate applies |

Varies; PayPal better for low-value |

| Chargebacks |

A$20–A$25 |

A$20 (with Radar: A$0.02/transaction) |

Up to 50% reduction via tools |

*Based on hypothetical scenarios like a Melbourne retailer (1,000 transactions: 70% domestic) or Brisbane cafe (A$35,000 monthly domestic). Actual savings depend on volume and mix.

PayPal shines for bootstrapped locals with easy plug-ins and charity rates (1.10% + A$0.30). Stripe excels for scalers with APIs, in-person payments (1.70% + A$0.10), and tools like Radar for fraud prevention—reducing losses by up to 20%.

Beyond Fees: The Integration Factor

Clunky systems hinder productivity and customer experience, but seamless integrations solve this by enabling real-time analytics, automated refunds, and GST compliance. Poor setups cause 20% cart abandonment—don't let that be you. PayPal offers quick WooCommerce/Shopify ties; Stripe's flexibility suits custom needs.

At C9, our collaborative approach ensures your gateway integrates flawlessly with existing operations, eliminating data silos and empowering data-driven decisions.

Which Gateway Wins for Your Business?

For local focus: PayPal minimizes upfront hassle. For growth: Stripe's lower fees and tools deliver superior ROI. Either way, custom integration unlocks full potential—streamlining processes, cutting costs, and boosting revenues.

Ready to optimise? Schedule a no-obligation discovery call with C9 today. We'll collaboratively assess your needs and craft a tailored path forward.

About C9

C9 is Australia's trusted partner in custom software, apps, integrations, and database development. From Sydney to Melbourne, we help businesses like yours harness technology for competitive advantage.

Return