Executive Summary

In short: Australian business owners and executives investing in bespoke custom software, mobile apps, system integrations, and database development are frequently missing a major opportunity. The R&D Tax Incentive offers eligible SMEs (aggregated turnover under $20 million) a 43.5% refundable tax offset (company tax rate + 18.5% premium) on qualifying experimental activities—effectively making the government a co-investor in your innovation. Many assume their projects don’t qualify, fear ATO scrutiny, or lack proper documentation, leaving significant cash refunds or tax savings unclaimed while operational costs rise and competitors advance.

What’s next? With EOFY 2026 fast approaching and FY26 activities in full swing, now is the time to evaluate your technology investments. Proper structuring and contemporaneous records can turn development spend into a strategic advantage for efficiency, profitability, and competitive edge.

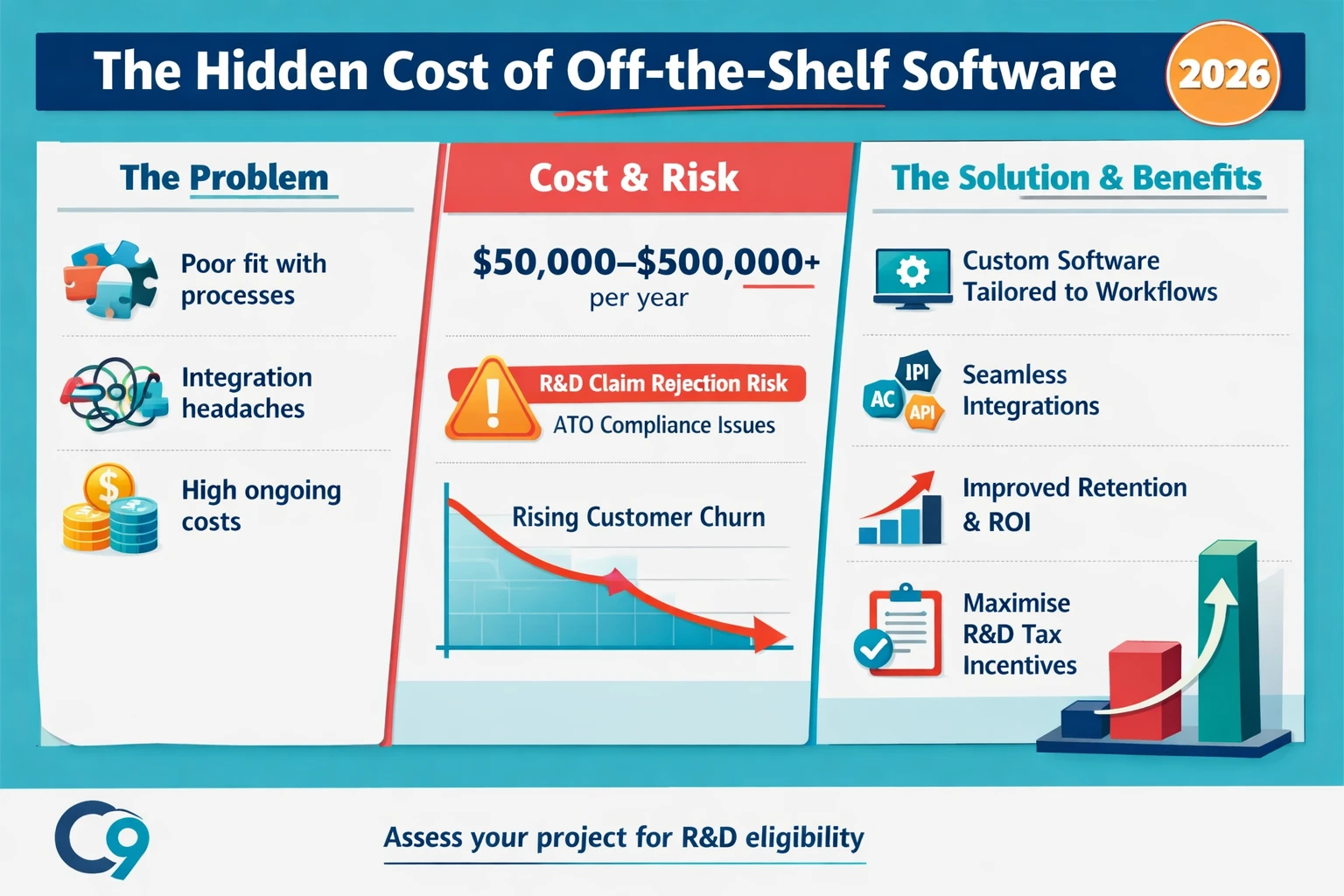

The Hidden Cost of “Standard” Software Solutions

As a detail-oriented Australian business executive, you know the frustration all too well. Off-the-shelf software rarely fits your unique processes. You invest heavily in custom bespoke software, purpose-built apps, complex integrations, or robust database solutions—only to face high costs, integration headaches, and systems that still fall short of driving the operational efficiency and revenue growth your business demands.

In 2026, these challenges are amplified. High operational costs eat into margins, outdated legacy systems hinder productivity, and competitors launch superior tech capabilities. Many businesses spend $50,000–$500,000+ annually on commissioned development without realising a substantial portion could qualify for the R&D Tax Incentive. Poor documentation or misclassified routine work risks ATO adjustments or rejected claims—especially with heightened compliance focus on the software sector. The result? Missed cash refunds, continued inefficiency, and lost competitive advantage.

At C9, Australia’s leading provider of custom software, apps, integration, and database development services, we partner with businesses to deliver tailored solutions that solve real problems while positioning projects for R&D eligibility where appropriate. This comprehensive guide equips you with the knowledge to assess your projects accurately, understand 2026 ATO expectations, and maximise legitimate benefits.

What Is the R&D Tax Incentive — And Why It Matters for Australian Businesses in 2026

The R&D Tax Incentive is jointly administered by the Australian Taxation Office (ATO) and the Department of Industry, Science and Resources (DISR). It encourages innovation by providing tax offsets on eligible R&D expenditure.

Key Facts for 2026 (SMEs with aggregated turnover < $20 million):

- Refundable tax offset: Company tax rate (typically 25%) + 18.5% premium = 43.5% effective rate for most eligible companies. Excess over tax liability is paid as a cash refund.

- Minimum expenditure: $20,000 (waived with registered research service provider).

- Maximum claimable: $150 million per year.

- Who qualifies: Australian-incorporated companies (sole traders, partnerships, and trusts generally ineligible).

- Registration: Via AusIndustry within 10 months of financial year-end (30 April 2027 for 30 June 2026 year-end).

In 2022–23, 12,956 companies claimed $16.2 billion in R&D expenditure, with small businesses comprising 46% of claimants (6,016 businesses). The professional, scientific, and technical services sector (including software) accounted for 44% of claims.

This is not a niche program for labs—it actively supports technology-driven businesses seeking efficiency gains and growth.

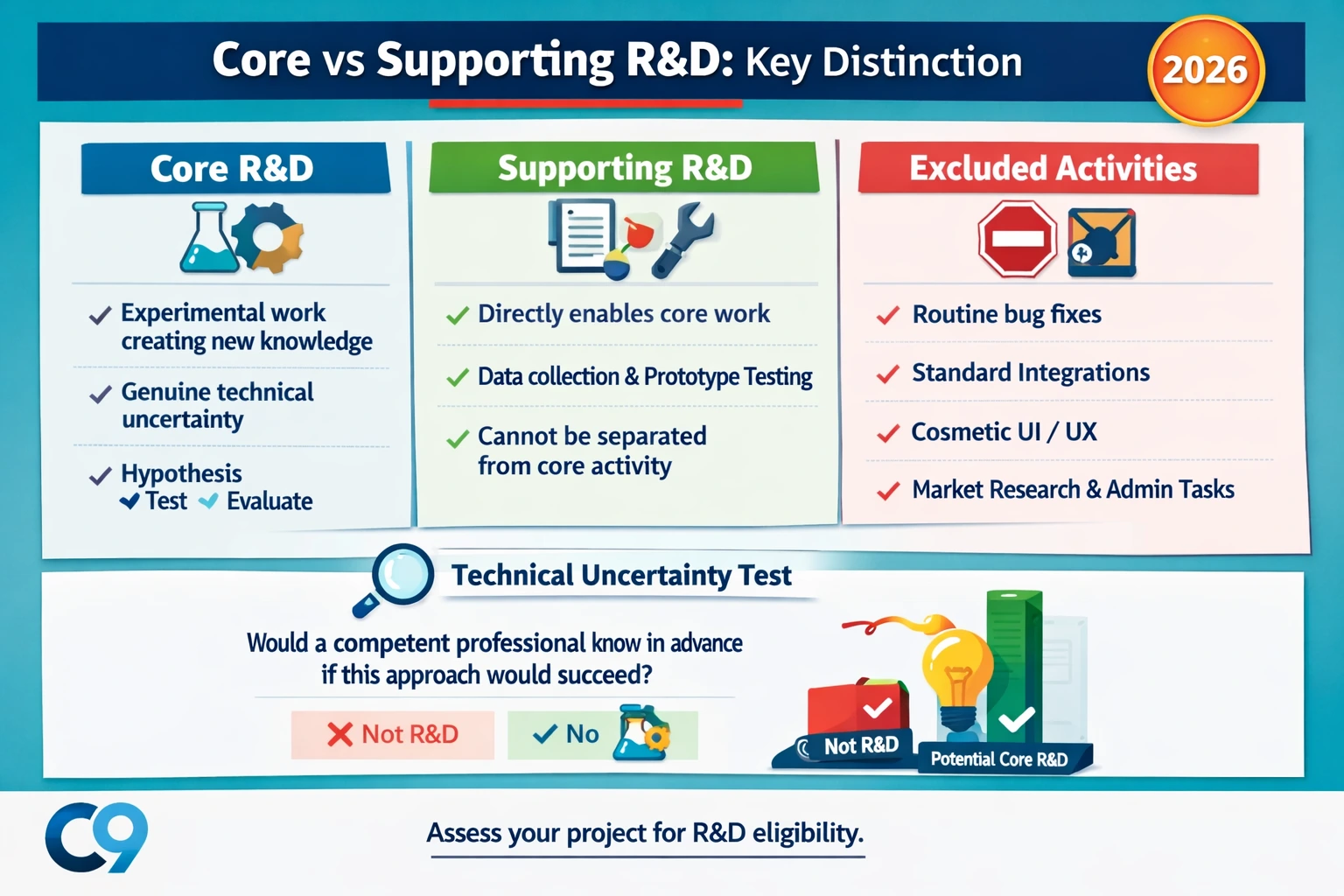

Core vs Supporting R&D: The Most Important Distinction

Understanding this separation is critical, as it determines eligibility and withstands ATO review.

Core R&D Activity: Experimental activities generating new knowledge (new or improved products, processes, or services) with genuine technical uncertainty at the outset. It requires a systematic approach: hypothesis, experimentation, evaluation.

Supporting R&D Activity: Directly supports core activities and cannot be separated (e.g., data collection, prototype testing, specific documentation).

Excluded Activities: Routine bug fixes, standard integrations using known methods, cosmetic UI/UX, market research, feasibility studies, or internal administration-dominant work.

The Technical Uncertainty Test (ATO’s key filter): Would a competent professional in the field know in advance if the approach would succeed? If genuinely uncertain, it may qualify.

Does Your Custom Software, Apps, Integration or Database Development Qualify?

This is the highest-intent question for executives commissioning bespoke solutions.

| Custom Software Activity |

R&D Eligible? |

Why / Why Not |

2026 ATO Risk Level |

| Novel algorithm or AI model with uncertain outcome |

Yes (Core) |

Genuine technical uncertainty; new knowledge via experimentation |

Low (if documented) |

| New architecture for unprecedented technical problem |

Yes (Core) |

Systematic testing of uncertain approaches |

Low-Medium |

| Novel data processing or database optimisation |

Yes (Core) |

Uncertain performance outcomes |

Low |

| Complex custom integration with no standard solution |

Possibly (Core) |

Only if beyond routine API work and technically uncertain |

Medium (fact-specific) |

| Prototyping & testing novel approaches |

Yes (Supporting) |

Linked to core activity |

Low |

| Standard API integration (e.g., Xero, Shopify) |

No |

Known techniques, predictable outcome |

N/A |

| Bug fixes, routine maintenance |

No |

Explicitly excluded |

N/A |

| Cosmetic UI/UX design |

No |

No new technical knowledge |

N/A |

| Data collection supporting core experiment |

Yes (Supporting) |

Inseparable from qualifying core work |

Low |

Real-World Examples for Australian Businesses:

- A manufacturer developing machine vision software for quality control with uncertain real-time accuracy.

- A retailer building a custom inventory system with novel optimisation algorithms.

- A service business creating AI-driven analytics integrations where performance in their environment is unpredictable.

Choosing a solution company should have collaborative approach incorporates hypothesis-driven development and logging that supports eligibility without compromising delivery excellence.

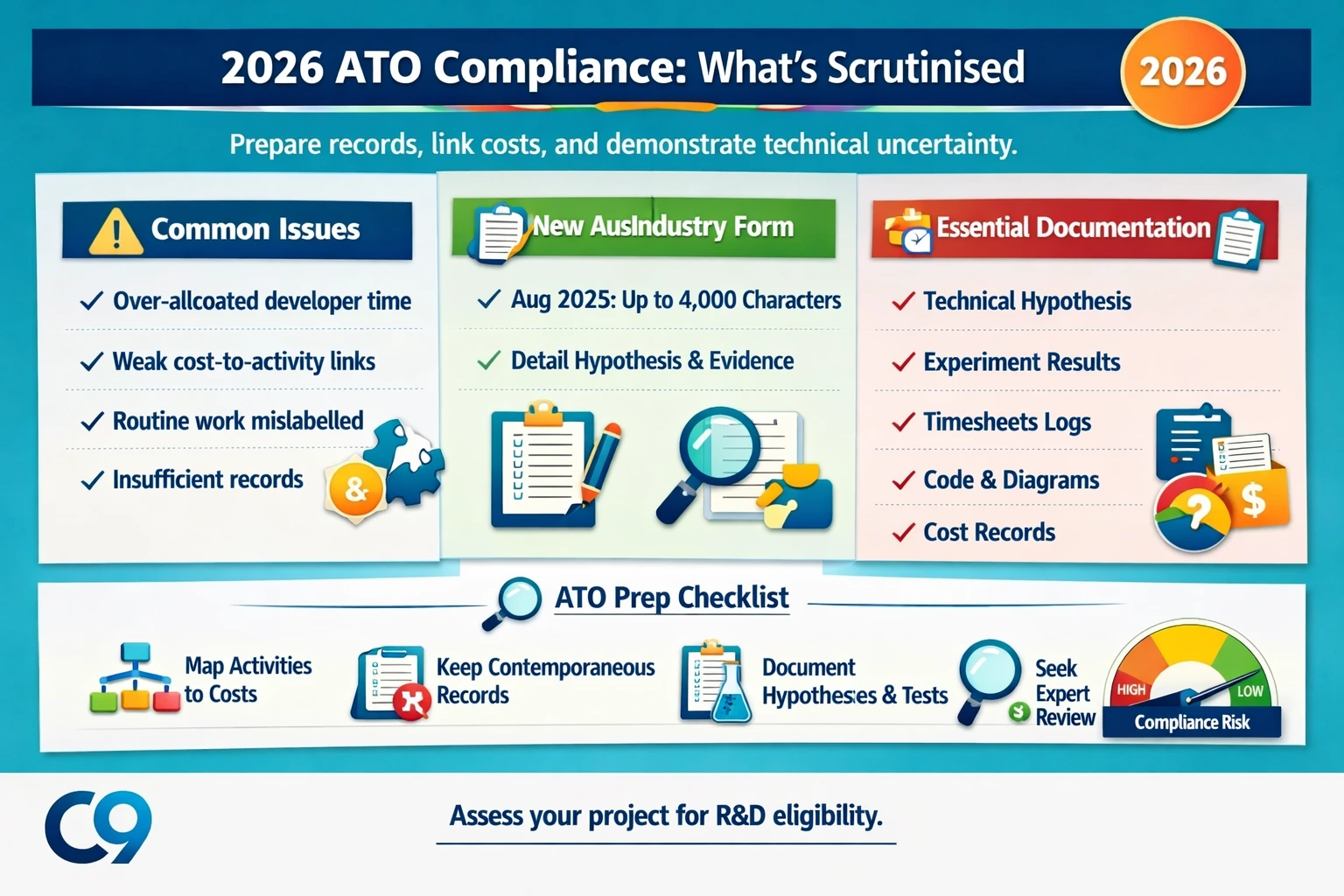

2026 ATO Compliance Environment: What’s Scrutinised and How to Prepare

The ATO has intensified focus on software claims due to their volume. Common issues include:

- Over-allocation of developer time to R&D.

- Weak linkage between costs and eligible activities.

- Routine development misrepresented as experimental.

- Insufficient contemporaneous records.

New AusIndustry Form (August 2025): Requires expanded detail (up to 4,000 characters for descriptions), hypothesis explanations, and documentation evidence.

Essential Documentation (Contemporaneous Records):

- Clearly defined technical hypothesis and uncertainty.

- Experimental method and results (including failures).

- Timesheets or commit logs.

- Technical outputs (code, diagrams, test results).

- Cost allocation trails (invoices, contracts).

Strong records protect your claim and demonstrate C9’s professional, trustworthy process.

Maximising EOFY 2026: Combining R&D with Instant Asset Write-Off (IAWO)

You cannot claim both on the same expenditure (per Section 355-205 ITAA 1997), but you can structure larger projects strategically.

Worked Example ($60,000 bespoke manufacturing software project):

- $18,000 infrastructure/setup → IAWO (immediate deduction).

- $12,000 standard UI/integration → General deduction.

- $30,000 novel machine vision algorithms → R&D Tax Incentive (~$13,050 benefit at 43.5%).

Total effective government support: Significant combined savings, lowering net cost and boosting ROI.

How C9 Structures Projects for Technical Excellence and R&D Eligibility

As your innovative, trustworthy partner, C9 builds bespoke custom software, apps, integrations, and databases with foresight. Our processes support hypothesis testing, detailed logging, and seamless delivery—helping you achieve operational efficiency, cost reduction, and revenue growth while maintaining audit-ready records where activities qualify.

We don’t just develop solutions; we collaborate to align technology with your strategic goals.

Stop settling for solutions that limit growth. With accurate understanding of the R&D Tax Incentive, proper documentation, and the right development partner, your custom software investments become powerful drivers of efficiency, profitability, and competitive advantage.

Ready to assess your project’s potential? Contact C9 today—Australia’s leading experts in custom software, apps, integration, and database development. Our team will discuss your needs, explore R&D opportunities, and deliver tailored, high-impact solutions before EOFY 2026. Let’s unlock your business’s full potential together.

Internal Links:

FAQ

Does custom software development qualify for the Australian R&D Tax Incentive? Yes—if it involves genuine technical uncertainty and systematic experimentation to generate new knowledge. Standard customisation, routine integrations, bug fixes, and UI design typically do not. Novel algorithms, architectures, or data methods often qualify when properly documented. Consult a registered tax adviser.

What is the R&D Tax Incentive rate for Australian SMEs in 2026? For eligible companies with turnover under $20M, it is generally the company tax rate (25%) + 18.5% premium = 43.5% refundable offset. Cash refunds possible if in loss position. Larger companies receive intensity-based non-refundable offsets.

What documentation does the ATO require in 2026? Contemporaneous records: hypothesis, experimental methods, time records, technical outputs, and cost trails. The updated AusIndustry form demands greater detail.

Can I combine Instant Asset Write-Off and R&D Tax Incentive? Not on identical expenditure, but different project components can use different treatments. Structure carefully with professional advice.

What is the FY26 registration deadline? For 30 June 2026 year-end: 30 April 2027 with AusIndustry. Documentation must be built during activities.

Data Sources (Verified for Credibility & Relevance as of May 2026)

Explore Related Insights on Custom Software Development Solutions

R&D Tax Incentive 2026: Is your custom software development eligible for a 43.5% tax offset?

EOFY 2026 Instant Asset Write-Off + Custom Software: What Every Australian Business Owner Must Know Before 30 June

AI-Powered Hyper-Personalisation in 2026: How Australian Enterprises Are Building Custom Software That Knows Your Customers

Why Sydney Businesses Are Switching to Custom Software Development

Your Competitors Are Making Their Core Software Smarter. What Are You Doing?

Why Melbourne Retailers Are Embracing Progressive Web Apps for Better Mobile UX – Insights from a Web Application Development Agency

Unlock the Power of Precision: How to Choose a Custom Software Development Partner in Australia: A Step-by-Step Guide for Executives

Navigating Australia's Tech Talent Crunch: How Skill Evolution is Reshaping Custom Software Development for Business Growth

The Generative AI Compliance Challenge: Building Secure, Ethical Enterprise Apps in Australia (Executive Guide)

Video Consultation Software Development: Building Secure Virtual Care Platforms

Unlock Efficiency: Why Progressive Web Apps (PWAs) and Hybrid Solutions Are Revolutionising Australian Businesses in 2026

Revolutionise Your Software Development: How AI-Powered Developer Collaboration is Boosting Australian Business Efficiency